History of accountancy

Gallery about the History of accounting

Origins[edit]

Early civilizations[edit]

Accounting is thousands of years old; the earliest accounting records, which date back more than 7,000 years, were found in Mesopotamia amongst the ruins of ancient Babylon, Assyria and Sumeria The people of that time relied on primitive accounting methods to record the growth of crops and herds. Because there is a natural season to farming and herding, it is easy to count and determine if a surplus had been gained after the crops had been harvested or the young animals weaned. Accounting evolved, improving over the years and advancing as business advanced.

Clay tokens, from Susa, Uruk period, circa 3500 BC.

Economic tablet, Uruk period (3200 BC to 2700 BC)

Early writing tablet recording the allocation of beer, Iraq 3100-3000 BC

Summary account of silver for the govenor, Iraq 2,500 BCE

Issue of barley rations, 2,350 BCE

Balance sheet Mesopotamia, 2040 BC (Ur III).

Accounting: distribution of food, first half of 2nd millenium BCE

Wooden brewery model (Middle Kingdom)... The rightmost figure with a tablet tucked under his arm is a scribe, counting the bottles.

Antiquity[edit]

The Res Gestae Divi Augusti (Latin: "The Deeds of the Divine Augustus") is a remarkable account to the Roman people of the Emperor Augustus' stewardship. It listed and quantified his public expenditure, which encompassed distributions to the people, grants of land or money to army veterans, subsidies to the aerarium (treasury), building of temples, religious offerings, and expenditures on theatrical shows and gladiatorial games. It was not an account of state revenue and expenditure, but was designed to demonstrate Augustus' munificence. The significance of the Res Gestae Divi Augusti from an accounting perspective lies in the fact that it illustrates that the executive authority had access to detailed financial information, covering a period of some forty years, which was still retrievable after the event. The scope of the accounting information at the emperor's disposal suggests that its purpose encompassed planning and decision-making.

Account of the construction of Athena Parthenos by Phidias

Roman writing tablet

Res Gestae

Edict on Maximum Prices, 301

Early accounting systems[edit]

The Heroninos Archive is the name given to a huge collection of papyrus documents, mostly letters, but also including a fair number of accounts, which come from Roman Egypt in 3rd century AD. The bulk of the documents relate to the running of a large, private estate is named after Heroninos because he was phrontistes (Koine Greek: manager) of the estate which had a complex and standarised system of accounting which was followed by all its local farm managers.

Bill of sale for a donkey

John Rylands University Library papyrus collection includes religious, devotional, literary and administrative texts.

Each administrator on each sub-division of the estate drew up his own little accounts, for the day-to-day running of the estate, payment of the workforce, production of crops, the sale of produce, the use of animals, and general expenditure on the staff. This information was then summarized as pieces of papyrus scroll into one big yearly account for each particular sub—division of the estate. Entries were arranged by sector, with cash expenses and gains extrapolated from all the different sectors. Accounts of this kind gave the owner the opportunity to take better economic decisions because the information was purposefully selected and arranged

Medieval[edit]

.jpg/94px-Einnahmenabrechnung_(1350).jpg)

Invoice 1350

.jpg)

Modern history[edit]

Early accounts served mainly to assist the memory of the businessperson and the audience for the account was the proprietor or record keeper alone. Cruder forms of accounting were inadequate for the problems created by a business entity involving multiple investors, so double-entry bookkeeping first emerged in northern Italy in the 14th century, where trading ventures began to require more capital than a single individual was able to invest.

Renaissance[edit]

In the 15th century double-entry bookkeeping was first codified by the Franciscan Friar, Luca Pacioli. In deciding which account has to be debited and which account has to be credited, the golden rules of accounting are used. This is also accomplished using the accounting equation: Equity = Assets − Liabilities. The accounting equation serves as an error detection tool. If at any point the sum of debits for all accounts does not equal the corresponding sum of credits for all accounts, an error has occurred. It follows that the sum of debits and the sum of the credits must be equal in value.

- Documents

Ledger, 1477

Genua Libro delle Colonne, 1485 (1)

Genua Libro delle Colonne, 1485 (2)

- Bookkeeping system by Johann Gottlieb, 1546

Johann Gottlieb was a merchant from Nuremberg, who traded in Venice. He wrote a treatise on double-entry bookkeeping in 1531, and an other book in 1546 both published at Nuremberg. These were the first books on bookkeeping in Germany and popularized the system of double-entry bookkeeping in Northern Europe. In his 1531 book Gottlieb mentions that there are different kinds of businesses and different kinds of systems of bookkeeping, meaning that there are various ways to arrange accounting records (Lee, 1990 p.364)

"Jornal oder Teglich Buch/ des ersten Buchhaltens"

Journal

"Schuldbuch"

Register of debts

Development of cash position

"Guterbuch"

"Aus dem folgendem Außzug oder vberkerich"

Closure of accounts

"Jornal auff Factorey/ des andern Buchhaltens"

Journal

"Schuldbuch"

Register of debts

Development of cash position

"Guterbuch"

"Folgen die uberbleibling"

Closure of accounts

- People on the job

Luca Pacioli, 1495

1517

1529

17th century[edit]

- Documents

Ledger, 1683

- People on the job

1655

The Account Keeper, 1656

1698

18th century[edit]

- Documents

1726

Ledger 1754-55

Invoice 1760

Invoice 1782

- People on the job

1713

1718

1745

1754

1756

Schreibende Kaufmannsfrau, 1772

That accounts for it 1799 caricature

19th century[edit]

The development of joint-stock company created wider audiences for accounts, as investors without firsthand knowledge of their operations relied on accounts to provide the requisite information. This development resulted in a split of accounting systems for internal (i.e. management accounting) and external (i.e. financial accounting) purposes, and subsequently also in accounting and disclosure regulations and a growing need for independent attestation of external accounts by auditors.

Books about bookkeeping[edit]

1816

1877

Diagrams picturing factory accounting, 1880s-90s[edit]

Books and Forms used in connection with Wages, 1889.

Books and Forms used in connection with Stores, 1889.

Books and Forms used in connection with Prime Cost, 1889.

Books and Forms used in connection with Stock, 1889.

Diagram of Manufacturing Accounts, 1896.

Documents[edit]

General ledger, 1828

Watson family slave account entry 1858-05-10

Ledger of the fur trader Dedo from Leipzig, 1876-1885

Ledger of the fur trader Dedo from Leipzig, 1876-1885

19th Century Business Day Book

Invoices[edit]

Invoice forms in the 1870s started to bear fine images of the company's factory, office-building and/or sales facility. An early example of an illustrated invoice is the Adler Rechnung Stephenson 27081835, an invoice from 1833 for the first steam locomotive in Germany, Adler of the Bavarian Ludwig Railway, made out from the locomotive manufacturer Robert Stephenson and Company.

1803

1803

1815

1833

1840

1867

.jpg/120px-Doflein_%26_Lefloch%2C_Paris%2C_Rue_Sèvignè%2C_1868_(Doit.).jpg)

1868

1870

1883

1885

1887

1878

1885

1889

1892

1893

1893

1894

1896

1897

1897

1897

1898

1898

1898

1899

1899

.jpg)

People on the job[edit]

1868

Chinese accountants at work in their store in San Francisco, 1892

BYU Bookkeeping 1895

20th century[edit]

Automation[edit]

Old burroughs adding machine, 1890

Elliot-Fisher book typewriter, 1903

Powers-Samas accounting machine

Buchungsautomat Anker BN 800 DZM

Accounting machine, 1931

Early SSA accounting operations, 1937

Electronic Recording Machine, Accounting wiring, 1950s

Powers-Samas Cards, 1954

IBM 403 Accounting Machine, 1960s

IBM 407 accounting machine at US Army, 1961

Diagrams[edit]

Prime expenditure divisions of a factory, 1905.

Principles of Organization by Production Factors, 1910.

Systems of Controlling Accounts, 1910.

Documents[edit]

1901

1909

Ledger, 1910

Account book, 1914

Cash book, 1921

Ledger, 1933

1964

Invoices[edit]

- 1900s

1900

1900

1901

1901

1901

1902

1903

1904

1904

1905

1905

1906

1906

1906

1906

1906

1906

1907

1908

1908

1908

1908

1908

1909

1909

1909

- 1910s

.jpg/98px-Abrechnung_C._M._Lampson_%26_Co_an_den_Silberfuchszüchter_Dalton_(1910).jpg)

1910

1910

_%2C_um_1910._600dpi.jpg/120px-Hannoversche_Gummi-Kamm_Co.%2C_Hannover-Limmer%2C_Rechnung_(Ausschnitt)_%2C_um_1910._600dpi.jpg)

1910

1910

1911

1912

1913

1913

1913

1913

1913

1914

1914

1915

1915 (1)

1915 (2)

1915

1918

1919

.jpg)

_,_um_1910._600dpi.jpg)

- 1920s

1921

1922

1922

1922

1922

1923

1923

1924

1927

- 1930s

1930

1930

1932

1932

1933

1934

1935

1935

1935

1935

1936

1936

1937

1937

1938

.jpg/120px-Account%2C_face_(West_Gloucestershire_Power_Company).jpg)

1939

.jpg)

- 1940s

1940

1943

1946

1946

1946

1947

1947

1948

1948

1948

1948

1948

1949

1949

- 1950s

1950

1950

1951

1951

1952

1956

People on the job[edit]

Elmer Candy Co Inc Office New Orleans, 1917

Grossman-Weinfeld Millinery Accounting Office NOLA, 1917

Hernsheim Cigars Accounting Office NOLA, 1917

National Lead NOLA Accounting Office, 1917

Southern Pacific RR Misc Accounts Office NOLA, 1917

Accounting machine, 1931

Early SSA accounting operations, 1937

.jpg/120px-Chullora_Railway_Canteen_-_patrons_paying_at_the_cash_register_(8078937890).jpg)

1944

IBM 403 Accounting Machine since late 1940s

1950

1951

1952

1953

1953

1953

1953

1953

1953

1953

1953

1953

1955

1955

1955

1955

1955

1956

1956

1959

1960

1961

1961

1962

1962

1966

1973

1985

.jpg)

21st century[edit]

Accounting software screenshots[edit]

Accounting software is application software that records and processes accounting transactions within functional modules such as accounts payable, accounts receivable, payroll, and trial balance. It functions as an accounting information system. It may be developed in-house by the company or organization using it, may be purchased from a third party, or may be a combination of a third-party application software package with local modifications. It varies greatly in its complexity and cost.

DCFM Calculator

Dette

Eqonomize

Ezersky

GnuCash

Grisbi

Homebank

KMyMoney

Np5

Npss

ROSA

Diagrams[edit]

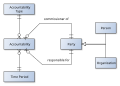

Accountability

Accountability and Legitimacy

Accounting cycle

Accounting documents

Clinical audit cycle

CSR framework - value1

GPK Marginal Cost Flow

IFAC Definition of MA

Material Flow Accounting Scheme

Development Managerial Costing

MCCF v2

.svg/120px-MediaWiki_1.19_database_schema_(r102798).svg.png)

MediaWiki database schema

Prozessablauf bei Finetrading

Accounting information systems

Zatrata

.svg)

References[edit]

This gallery incorporates material from Wikipedia articles on: accounting, accounting software, and double-entry bookkeeping system.

- Thomas Alexander Lee (1990) The Closure of the accounting profession - Volume 1.